Scotttheking kicked this off last year. Not seeing it yet so figured lets get the party started.

So, 2024 happened, you can look up your previous posts below. How did your 2024 come out and thoughts on your 2025?

Past threads:

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2023

2024

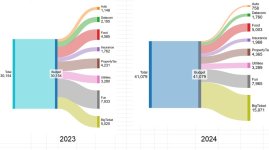

Not a formatting whiz at Ars so hopefully the 2023 review and 2024 forecast at the bottom there worked out ok. I was uh, wrong about about 2024 - I called for 5% but ended up -1.2%. The vast bulk of that was mark to market on fixed income lower on higher rates and gbp outperforming euros, the stocks were pretty flat'ish. Not a great year but not fussed.....wouldn't have minded some of that 20% up US stock action but that isn't what we tend to hold due to taxation issues.

2025, hoooo boy, uh, my hunch is the trump shitshow is going to be inflationary and rates on the longer end (regardless of what the fed does on the fed funds rate which is all they can directly control) will trend higher so I am looking at another year of bond/dividend income with mark to market temporary 'loses' on existing bond holdings. I project 0%. My other hunch, gold goes and hits 3500 if not approaching 4000.

Buckle up people.

What say ye?

So, 2024 happened, you can look up your previous posts below. How did your 2024 come out and thoughts on your 2025?

Past threads:

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2023

2024

Not a formatting whiz at Ars so hopefully the 2023 review and 2024 forecast at the bottom there worked out ok. I was uh, wrong about about 2024 - I called for 5% but ended up -1.2%. The vast bulk of that was mark to market on fixed income lower on higher rates and gbp outperforming euros, the stocks were pretty flat'ish. Not a great year but not fussed.....wouldn't have minded some of that 20% up US stock action but that isn't what we tend to hold due to taxation issues.

2025, hoooo boy, uh, my hunch is the trump shitshow is going to be inflationary and rates on the longer end (regardless of what the fed does on the fed funds rate which is all they can directly control) will trend higher so I am looking at another year of bond/dividend income with mark to market temporary 'loses' on existing bond holdings. I project 0%. My other hunch, gold goes and hits 3500 if not approaching 4000.

Buckle up people.

What say ye?

Last edited by a moderator:

") ), but I'm ok with taking on mortgage if the bubble ever pops and we can afford something. SUCCESS!

), but I'm ok with taking on mortgage if the bubble ever pops and we can afford something. SUCCESS!